The vibrant culture of food trucks is not just about delicious eats; it’s also about convenient payment methods. As food trucks increasingly pop up in urban centers, understanding whether they take cash becomes critical for enthusiasts and consumers alike. In this exploration, we will dive into the cash landscape within the food truck industry, revealing the benefits, economic implications, and evolving trends in payment acceptance. Each chapter contributes to a comprehensive understanding, from the historical significance of cash transactions to the rise of digital payments, consumer preferences, and future projections. Let’s uncover this delectable intersection of food and finance that appeals to everyone—from hobbyists to global fans.

Cash on the Curb: Navigating the Cash Question in the Food Truck Era

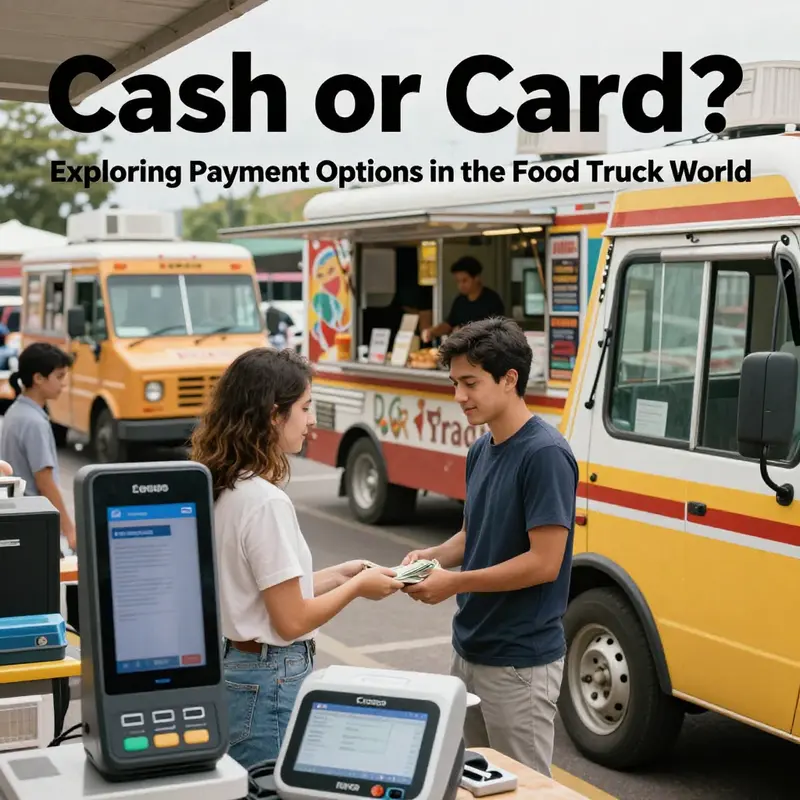

On a sunlit afternoon, as the grill sizzle and the line of hungry orders snakes around a cluster of bright carts, a question lingers like steam above the griddles: do food trucks take cash? The answer is not a simple yes or no. It is a nuanced picture of a payment landscape that sits at the intersection of tradition and technology. In many corners of the street food world, cash remains a practical and familiar option that works for both vendors and customers who carry coins or folded bills. Yet the same scene that loves cash is increasingly sheltered by screens and chips, as vendors adopt electronic payment systems that promise speed, accuracy, and cleaner books. The result is a marketplace where cash and digital methods coexist, each appealing to different needs and moments in the day.

That coexistence is grounded in economic realities. Cash payments tend to incur lower or negligible transaction costs for the seller, compared with the fees charged by card processors. For operators who pivot from one event to the next, such as farmers markets, office blocks, or late night food courts, accepting cash without investing in hardware or connectivity can be a straightforward bottom line decision. In the lean world of mobile food service, where margins are tight and every portion of revenue matters, avoiding monthly fees and per transaction charges can be as important as the flavor of the stew. The cash draw, the change tray, the simple tally at the end of a busy shift all echo a philosophy of minimal friction and direct money changing hands.

But cash is not simply a relic. It is a bridge to accessibility. Not everyone carries plastic or trusts online portals with transaction details or privacy. For customers who want to pay without the risk of a failed signal, who may be traveling with limited data plans, or who prefer to tip in a way that feels immediate and personal, cash remains the most intuitive option. Even among those who regularly use cards or digital wallets, cash offers a sense of control during a high speed purchase: you hand over the money, you receive the product, you are done. In such moments, the simplicity of cash can feel almost ceremonial, a nod to the days when the only way to sample a new neighborhood culinary idea was to reach into a pocket and hand someone the exact amount.

Yet the movement toward electronic payments is steady and undeniable. Mobile point of sale solutions have evolved from clunky add ons to elegant, integrated systems that fit into a truck’s compact footprint. They promise faster checkouts, more accurate receipts, and better data collection for both operator and customer. The modern cart often accepts a spectrum of options beyond cash: magnetic stripe cards, chip enabled cards, contactless cards, and a range of digital wallets that readers recognize without demanding a signature on a pad the size of a menu. The shift is not about forcing customers to switch, but about giving them a choice that aligns with how they prefer to pay in that moment. This evolution mirrors broader retail trends where speed, convenience, and data capture become part of the service experience.

For vendors, the decision to go cashless or stay cash friendly depends on location, event type, and crowd dynamics. Outdoor festivals with poor network coverage can push operators toward offline cash processing, while in other settings the crowd may expect quick digital options and receipts. The ability to record every sale, automate inventory updates, and easily reconcile accounts adds a level of operational clarity that many operators find compelling. The research landscape around food truck payments consistently highlights this tension: many vendors still rely on cash, but more and more have begun to integrate digital payment options as a core part of their business model because the benefits extend beyond speed to loyalty, marketing, and financial planning.

Beyond the financial calculus, the social rhythm of the food truck encounter plays a crucial role. People gravitate toward the kitchen window not just for flavor, but for the interaction and trust that comes with giving cash directly to the cook, and the immediacy of a tip. Cash preserves a tactile culture of street dining. Still, the rise of digital systems promises a different kind of social signal. A tap or a wave of a phone can feel intimate when a customer is greeted with a friendly receipt and a loyalty point earned or a future discount promised. This is not a battle of cash versus card; it is a negotiation of experience, the tempo of service, and the clarity of records that help people remember where they spent their money and what they enjoyed most.

As the landscape evolves, many operators maintain a hybrid approach that preserves the benefits of cash while offering digital options when opportunities arise. For readers planning visits to food trucks, the practical advice is straightforward: check ahead for payment terms at events with large attendance or limited on-site facilities, read the signs at the window, and when in doubt ask the staff. In most cases, the choice you make—cash or digital—reflects a moment’s convenience, a desire to support a local chef, or a preference for a particular kind of customer experience. The broader takeaway is that cash remains an essential option in the spectrum of payment methods, even as the momentum toward digital solutions gathers pace. The street-food payment landscape continues to evolve with each new window opened and each new screen activated, shaping how we pay, tip, and remember the meals that travel from fire to feast.

External resources can deepen this understanding. For readers who want a broader industry-wide view of how food trucks balance cash and digital payments, a recent feature on mainstream food media provides a concise synthesis of current practices and the rationale behind them. It emphasizes the practicalities of card processing, the importance of reliable connectivity, and the strategic value of offering multiple payment pathways to customers. It complements the nuanced, ground-level observations in this chapter and helps readers see how the micro-level decisions of individual vendors fit into a larger ecosystem of street food, small business finance, and consumer expectations.

From Cash Bags to Cloud Payments: Navigating the Cash–Electronic Payment Divide in Food Trucks

In the fast lanes of a bustling street, the old and the new collide at every window. A line of hungry patrons waits as a grill sizzles, and a mobile business adapts in real time to what customers bring to the window and what the market demands. The central question—do food trucks take cash?—unfolds into a larger story of how mobile operations balance tradition with technology. Cash remains a resilient option for reasons of accessibility, speed, and reliability in areas with spotty card networks or banking access. But momentum toward electronic payments is undeniable, with mobile POS devices enabling credit and debit cards, digital wallets, and contactless options. The benefits include faster checkouts, real-time sales reporting, inventory visibility, and improved security. For customers, digital payments offer convenience and the security of not carrying large sums of cash, while cash maintains speed and inclusivity for those who prefer it. Operators weigh costs—card processing fees and platform charges—against revenue uplift and operational simplicity. The best models blend both worlds: offering a cash option while providing an electronic system that streamlines checkout, improves record-keeping, and scales across locations. Regulators and communities shape the landscape, highlighting the need for clear fee structures, licensing, and compliance. In this balanced view, cash and electronic payments are not enemies but complementary tools that help food trucks compete, adapt, and grow in a mobile, multi-site world.

Economic Calculus on the Curb: Why Cash Still Shapes the Bottom Line for Food Trucks

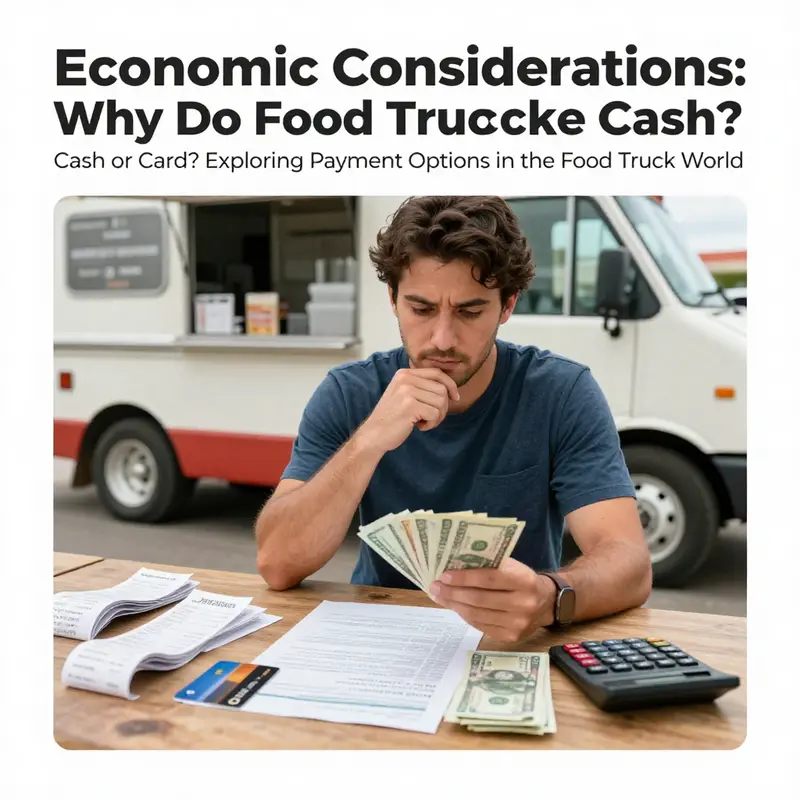

In the street-food economy, money moves with a rhythm all its own. The curb becomes a daily ledger, and the health of a mobile kitchen is often measured not only by flavor but by the flow of payments. Cash remains more than a relic of the past; it is a deliberate economic choice shaped by margins, risk, and the pace of service. For many operators, cash is a quiet ally that helps the operation stay alive on the road, especially on peak days when lines string out and every minute of service matters.

At the heart of the cash-versus-card decision is a straightforward but consequential idea: transaction costs. When a customer pays with a card, the merchant pays a processing fee to a bank or payment processor. Those fees typically sit in a range from roughly 1.5% to 3.5% per sale. For a small, margin-tight operation, those fractions can accumulate quickly. Consider a truck that grosses five hundred dollars in a busy shift; a two percent processing fee reduces that gross by ten dollars. Over time, repeated reductions of this kind nibble away at profits that would otherwise cover groceries, fuel, or a new oven for the kitchen on wheels. For operators who are still building a cushion, every percentage point matters because it translates into real resources—gas, ingredients, a newer grate, or more reliable equipment.

This arithmetic helps explain why some food trucks pursue a cash-only model. By removing card processing entirely, they preserve more of each sale and sidestep ongoing charges that quietly erode margin. The appeal is most acute for the smallest operations, where a single busy weekend can tilt the annual balance sheet. Yet even in cash-first setups, there is a balance to strike. Cash is simple and immediate, but it carries its own set of responsibilities: securely storing bills, counting at close, reconciling cash drawers, and guarding against tampering or theft. In practice, many operators find that the bottom line improves when they marry the two approaches—keeping cash as a core, predictable element of revenue while embracing digital payments to capture a broader customer base.

Alongside the economics are the realities of cash flow. Cash arrives in hand immediately, with no waiting period for electronic settlements to post. This immediacy can be a lifeline for a mobile business that must translate daily receipts into fresh ingredients, fuel, and wages in real time. The daily rhythm becomes more predictable when the cash portion of sales is predictable too. In such a setup, management can steer the business with a tighter sense of liquidity, which helps when a truck stops at a festival or popup where cash-only lines still rule. For operators weighing this choice, it helps to remember that cash and digital payments do not have to be mutually exclusive. A hybrid approach preserves liquidity while offering speed and convenience to customers who prefer or require electronic payments.

The customer perspective adds another layer to the calculation. Cash remains appealing to segments of patrons who either do not carry cards, are wary of fees, or simply prefer the tangible nature of handing over physical money. In markets with uneven access to banking or where digital infrastructure is spotty, cash ensures access and inclusivity. On the other hand, there is a growing population of customers who expect speed and digital convenience. They favor tap, scan, and wallet payments because they are quick, traceable, and easy to budget for. For many operators, the optimal strategy is to offer both options, cleverly directed by the context of the day and the crowd gathered around the truck. When events organize a cashless posture or when time is at a premium, a robust digital option can keep lines moving and reduce the likelihood of frustrated customers abandoning the queue.

Operational realities reinforce this blend. Cash handling requires secure storage, regular counting, and disciplined reconciliation. It invites the possibility of counterfeit notes, errors in change, and the need for reliable cash drawers and staff training. Electronic payments shift much of that burden toward software-driven settlements, real-time reporting, and automated inventory tracking. The trade-off is the cost of hardware, connectivity, and maintenance, plus ongoing training to ensure staff can operate devices with confidence during busy service windows. In practice, the most resilient operators design a payment ecosystem that minimizes risk while maximizing access and speed. They set clear procedures for cash drops, end-of-day reconciliation, and regular audits, and they implement digital tools that smooth the flow of data from sale to analysis. This approach helps ensure that neither the cash nor the digital channel becomes a bottleneck for growth.

Beyond the mechanics, the choice of payment methods intersects with business identity and strategic planning. A cash-forward posture can signal simplicity and low overhead to market neighbors and regulators, while a modern hybrid system communicates adaptability and scalability. For entrepreneurs who spend long hours on the road, that adaptability is the core advantage. It allows them to pivot—from a neighborhood market to a large festival or a food hall—without sacrificing either margins or customer reach. The key is to calibrate the mix to the location, the audience, and the event’s tempo. In practice, it is not about choosing cash over digital in absolute terms; it is about choosing the right mix for the right moment, and then adjusting as experience and data accumulate.

Those who seek a deeper understanding of how payment choices interact with the broader legal and regulatory framework may find value in exploring the legal considerations for Latino food truck startups. This resource provides context on how licensing, taxes, and local rules shape—and sometimes constrain—payment strategy on the curb. You can read more here: Legal considerations for Latino food truck startups.

As the landscape evolves, many operators discover that the path to sustainable growth lies in embracing the strengths of both worlds. The most successful trucks design payment experiences that are fast, transparent, and customer-friendly, while maintaining tight control over costs and cash flow. They recognize that a cash-forward baseline offers stability in volatile markets and for truly lean operations, but a digital layer opens doors to new markets, better data, and more flexible staffing. The overarching lesson is that payment strategy should be treated as a core component of unit economics, not as an afterthought or a separate facet of operations. When viewed as an integrated system, the choice between cash and digital becomes a matter of strategic timing and disciplined execution rather than a binary stalemate.

For readers looking to anchor these insights in a practical framework, the essential idea is to manage cash flow with intention. Track the true cost of every payment method, including the incremental hours spent handling cash and the potential revenue lift from offering digital options. Consider the geography and the venue calendar, because some locations lean cash-heavy while others favor fast digital transactions. Above all, maintain an ongoing dialogue with staff about how to handle money efficiently and safely, and adjust the payment mix as the business grows. Finally, for a structured overview of how cash flow management fits into small-business operations, consult the U.S. Small Business Administration’s guidance on managing cash flow: https://www.sba.gov/business-guide/finance-and-operations/manage-your-cash-flow

Cash, Cards, and Convenience: How Consumer Preferences Shape Payment at Food Trucks

Across the curbside world of sizzling grills and aromatic steam, the way customers pay is as much a part of the experience as the flavor on the plate. For many diners, money changes hands as effortlessly as a conversation with the cook, yet the method of payment quietly signals a lot about speed, transparency, and personal preference. Do food trucks take cash? The short answer is yes, they often do. The longer, more nuanced answer reflects a street-level economy in which cash remains a practical, even beloved, option for a substantial slice of the public. Recent data from the National Food Truck Association illuminate a shifting landscape: more than two-thirds of trucks now accept credit and debit cards, thanks largely to the rapid spread of mobile point-of-sale systems that turn a smart device into a full-service register. Those systems do more than process a card; they streamline the entire transaction, create an electronic record, and often nudge a tip in a way that feels natural within the service culture. Yet this embracing of digital payments does not erase the enduring appeal of cash. The grease and grit of the street vendor economy have a durability that cash helps preserve, especially in places where crowds surge and lines move quickly, or where customers arrive with pockets full of small denominations that seem tailor-made for a quick bite between errands. The tension between cash and card, between old habits and new technologies, is not a controversy but a continuum. It is a continuum that reveals much about consumer psychology, vendor economics, and the evolving etiquette of tipping and service in fast, affordable food.

To understand why cash still holds a foothold, it helps to look at the practical calculations food truck operators face every day. Cash is simple on the surface: it has no processing fees, no monthly service charges, and no per-transaction costs that chip away at low menu prices. For trucks that keep pricing intentionally lean, paying for a card reader or a full mobile POS system can squeeze margins, especially during peak festival seasons or in neighborhoods where foot traffic shifts with the weather. For operators balancing the thin margins of a small, mobile business, every penny matters. Cash can also reduce the anxiety of customers who are wary of digital wallets, or who simply value the tactile certainty of folding cash in a hand and walking away with a meal in seconds. In this way, cash acts not merely as a form of payment but as a signal of accessibility. It tells customers that the truck recognizes diverse economic realities and strives to accommodate them in real time.

Still, the economics of cash acceptance are not the only factor at play. The digital transition in mobile food service has introduced benefits that cash alone cannot deliver. Card-based transactions produce clean, auditable records that help with inventory control, revenue tracking, and tax compliance. They can also open the door to faster service, especially in high-traffic settings where every second saved at the register translates into more meals served. Modern mobile POS platforms often integrate gratuity prompts, which serialize the tipping culture so common in hospitality into a seamless, optional, and non-intrusive step at the end of a purchase. From a customer’s perspective, this can feel like a natural extension of good service. From a vendor’s perspective, it offers a predictable way to acknowledge labor and maintain a fair compensation flow for the team. The result is a nuanced ecosystem where the convenience of the consumer and the practicalities of the vendor meet in a single transaction.

The research paints a picture of a landscape that is neither uniformly cash-first nor uniformly card-first. While 68 percent or more of trucks have adopted card acceptance, cash remains a steadfast alternative, particularly in certain contexts. High-traffic urban corridors, outdoor festivals, and local markets often draw crowds who favor speed and privacy. In such environments, a cash transaction can feel instantaneous: hand over the money, receive your receipt, and move along the curb with minimal friction. There is also a social element to cash that resonates with some communities, where the act of paying with cash carries a sense of tangibility and control that digital methods do not fully replace. The persistence of cash in these settings underscores an important point: consumer convenience is not a single path, but a constellation of options that communities, cultures, and occasions shape in unique ways.

In practice, the presence of cash on the menu is rarely a stubborn directive, but more often a visible preference that communicates inclusivity and pragmatism. Many trucks post a straightforward sign that says “Cash Accepted” or “Card Preferred,” offering a quick cue to customers about what to expect. These on-site signals matter because they empower people to decide how they want to pay before they approach the line, reducing the likelihood of delays or frustration. And for customers who rely on cash for privacy, speed, or simple habit, these on-site cues are a welcome acknowledgment that the street is a space where diverse payment cultures can coexist. The everyday choice to carry cash or to rely on a digital wallet has become a statement of personal agency, one that fits into the broader rhythm of city life and the seasonal rhythms of street commerce.

From the operator’s vantage point, managing cash as a payment option requires a blend of discipline and hospitality. Handling cash means careful counting, secure storage, and timely banking to ensure cash flow remains predictable. It also means clear policies for change, refunds, and the handling of tips. Some vendors may find that integrating tipping features into digital payments helps standardize the hospitality ethic across shifts and teams, while still supporting customers who pay with cash. These practices, over time, can strengthen the relationship between truck and patron by aligning expectations and reducing friction. They also lay a foundation for trust, which is a critical currency when the operation depends on repeat customers and the social energy of a busy market. As vendors experiment with different configurations of cash and card acceptance, the most successful models tend to be those that preserve speed, transparency, and warmth at the point of sale.

What does this mean for the average customer wandering through a food market or a neighborhood block party? It means options—and a quiet invitation to choose what feels most comfortable in the moment. Some shoppers value the immediacy of cash, appreciating the ability to finalize a transaction without waiting for a reader to verify a card or a connection to a payment network. Others seek the convenience of tapping a phone at the register, a gesture that can feel almost effortless and warrants a quick thank-you from a grateful cook. The tipping conversation, which has grown with digital payments, often nudges customers toward generosity by presenting gratuity as part of the transaction flow rather than an afterthought. In practice, this helps sustain the team behind the stove, which is a meaningful nod to the workforce that fuels the city’s street-food economy.

The evolving etiquette around payment methods also intersects with broader legal and regulatory considerations. For operators, understanding the basics—how to handle cash securely, how to issue legitimate receipts, and how to maintain accurate records for tax purposes—can be as important as choosing a payment technology. As communities grow more vigilant about consumer protections and financial reporting, the cash-versus-card decision becomes part of a larger conversation about compliance, transparency, and accountability. Operators who want to stay ahead of the curve may find value in proactive practices such as clearly labeling accepted methods, providing receipts, and maintaining tidy cash drawers that can be audited and reconciled with digital records. For readers who are thinking about starting a street-food venture, these considerations translate into practical routines that balance simplicity with responsibility. For those navigating the regulatory terrain of Latino food truck startups, the topic expands into a broader set of legal considerations that touch on licensing, tax compliance, and payment handling. See more in the linked discussion around the legal considerations for Latino food truck startups, which anchors the practical realities of cash and card use within the regulatory environment of mobile food commerce. legal considerations for Latino food truck startups

As payment technologies continue to evolve, so too will customer expectations. The rise of contactless options and streamlined digital wallets promises even quicker transactions and more precise data capture for vendors. Yet even as the convenience of these tools grows, it is improbable that cash will vanish from the food truck scene anytime soon. The street economy is built not on a single payment method but on a mosaic of preferences, shaped by place, moment, and lived experience. The best trucks understand this mosaic and design their service to honor it. They train staff to recognize when a patron would prefer cash for speed, when a customer might favor a card for a cleaner, traceable receipt, and when a digital wallet might be the most seamless choice for a quick bite on the go. The result is a service encounter that feels democratized, where everyone’s choice is respected, and where the food—the central attraction—remains the shared focal point.

In the end, the question “Do food trucks take cash?” operates on multiple levels. It is a question about payment mechanics, but it is also a question about access, convenience, and trust. It asks who gets to participate in the street-food economy and how that participation is expressed at the moment of purchase. It asks how vendors balance the friction of cash handling with the efficiencies of modern payment systems. And it asks what the customer experience should feel like when a simple meal is purchased in a bustling city corridor, under a sunlit awning, or at the edge of a weekend festival. The answer is not a single rule but a living practice, one that continues to adapt as communities, technologies, and commerce evolve together. For readers who want to explore related angles—how this payment mix plays out in different neighborhoods, or how operators balance cash flow with inventory and staffing—there are many stories that deepen this understanding, including resources that delve into the broader ecosystem of Latino street food and the ways owners navigate legal and operational challenges.

Further reading and context can be found through a broader lens on business and payments, which complements the street-level realities described here. For those who want to broaden their view of how communities engage with cash and digital payments in small, mobile businesses, the following external resource offers additional context and data: https://www.census.gov/topics/business-economy.html

Between Cash and Cloud: Navigating the Evolving Payment Landscape for Food Trucks

The question of whether food trucks take cash might seem simple at first glance, but it sits at the crossroads of habit, technology, and economics.

Cash remains a tangible, universally accepted medium that many customers rely on for quick, no-hassle purchases. Yet digital receipts, contactless taps, and mobile wallets are becoming more common on curbside service. In this shifting terrain, operators weigh the costs and benefits of keeping cash on the counter against investing in digital payment systems that promise faster transactions, clearer record-keeping, and better compatibility with tipping culture. The tension between cash and cloud is a spectrum along which many trucks now operate, often blending old-school pragmatism with new-age efficiency.

The current state of payments in the food truck sector shows a blended character. Industry data from relevant trade sources indicates a pivot toward card acceptance, with the majority of trucks now equipped to handle credit and debit transactions. Mobile card readers are common, portable, and sometimes include prompts for tips and digital receipts, shaping the social dynamic of the sale. The tipping conversation is evolving too: suggested tip amounts are visible at checkout, signaling alignment with formal dining expectations in a fast-paced setting. For customers who have long relied on cash, these prompts can feel like a nudge to redefine the social contract of street-service dining, while others see it as a sign of professional operation and fair compensation.

Into this landscape, the cash option remains a practical tool and cultural anchor. In resource-constrained environments, where digital infrastructure is patchy or card processing costs feel burdensome, cash ensures participation regardless of device access or network connectivity. The result is a hybrid model in which cash and digital payments coexist, each serving different customer cohorts and moments in the day. A lunchtime rush may favor cash for speed and universal access; a late-afternoon pickup near offices may lean toward card acceptance and smoother tipping. This coexistence helps operators manage risk and accommodates weather, location, and customer preference, showcasing the resilience of the food truck model.

Beyond operations, the economics of payment methods shape decisions. Processing fees, monthly platform charges, and hardware costs affect margins. Some operators go cash-only to avoid ongoing costs, while others invest in mobile payment infrastructure to streamline sales, improve accountability, and gain data for marketing and inventory planning. The economics are about more than cost reduction: digital systems can accelerate checkout, increase throughput, and enable precise revenue tracking and loyalty initiatives that may boost profitability over time.

Accessibility and customer experience are central. Those who favor contactless payments value speed, safety, and digital records; others prefer cash for its immediacy and budgeting simplicity. Clear explanations about accepted forms of payment and tipping practices, along with staff training for courteous handling of diverse payment styles, help maintain good customer relations. The best trucks communicate with signs, offer trained staff, and ensure everyone feels welcome, regardless of payment method.

Looking ahead, the trend toward digital and contactless payments will likely strengthen, while cash persists where trusted and familiar. The industry is normalizing digital tipping, streamlined receipts, and mobile readers that fit street hospitality workflows, but cash remains a reliable fallback. The future is not a single chosen path but a flexible ecosystem that respects diverse preferences, adapts to different neighborhoods, and preserves the nimble, people-centered ethos of street food. Operators who balance cash and digital options well become case studies in adaptability, combining reliability with data-driven advantages.

For readers curious about the human side of this evolution, the experiences of veteran operators offer instructive insights. Profiles of veteran food truck owners illuminate how relationships with customers, community, and cash culture survive or transform as digital tools gain traction. The narrative extends beyond technology to reflect the rhythms of city life on wheels. You can read more about these perspectives here: https://latinosfoodtrucks.net/profiles-of-veteran-food-truck-owners/.

In summary, the best trucks are the ones that communicate clearly, serve quickly, and respect diverse preferences. Whether customers hand over cash or tap a card, the aim remains the same: deliver good food with good service in a way that honors both tradition and innovation. The street remains a testing ground where reliability, empathy, and adaptability determine success, not ideology. The question do food trucks take cash becomes a practical inquiry about balancing a cash-based culture with a broader digital economy.

Final thoughts

The conversation surrounding cash payments in food trucks reveals much about the intersection of culinary arts and modern economics. As consumer preferences evolve, food trucks must adapt their payment systems to ensure convenience and accessibility. While cash remains a steadfast option for many, electronic payments are quickly gaining ground, reflecting a broader trend in the dining industry. This dynamic landscape suggests that food trucks will continue to be at the forefront of payment innovations while still catering to traditional cash users. As you venture out to savor delicious street food, remember the flexibility of payment methods enhances your experience.